Tokenized Real-World Assets in 2026: What's Actually Live, What's Still Pilot, and What Beginners Should Understand

Tokenized real-world assets are off-chain assets, such as funds, Treasuries, or gold, represented on a blockchain as digital tokens. Most explainers list the upside and skip the part that matters most for a cautious reader, which is what the token actually gives you and who has to make good on it.

Key Takeaways

- A tokenized real-world asset is usually a claim on an off-chain asset or fund, not the physical asset itself. Your rights depend on the legal wrapper, not on the blockchain.

- The most mature live categories in 2026 are tokenized money market funds, Treasury-backed products, and tokenized gold, with private credit and fund wrappers live but restricted to eligible investors.

- Broad retail tokenized stocks, most tokenized real estate, retail private equity, and deep 24/7 secondary markets remain limited, jurisdiction-specific, or pilot-stage.

- Tokenizing an asset does not automatically make it liquid, safe, directly owned, or exempt from securities law. Regulators treat a tokenized security as a security.

- Before trusting any RWA product, ask what the token represents, who holds the asset, who can transfer it, which record is authoritative, and how you exit.

Tokenized real-world assets are traditional assets, such as money market funds, short-term Treasuries, gold, private credit, or company shares, recorded and moved as tokens on a blockchain. The phrase covers a lot of ground, and that is exactly where beginners get lost. This guide follows Blockready's education-first method, which means explaining how tokenization works, what the token legally represents, and where risk still sits, before anyone decides whether an RWA belongs anywhere near a portfolio.

The 2026 headlines make this sound settled. In practice, the live market is narrower than the narrative, and the token is rarely the same thing as the asset it points to. If you keep one question in mind while reading, make it this one. What claim does the token actually give me, and who enforces that claim when something goes wrong?

What a tokenized real-world asset actually is

A real-world asset, in crypto usage, is an off-chain asset or financial claim represented on-chain through a token. That off-chain source can be a Treasury bill, a fund share, a gold bar, a private loan, or a share in a company. The token is a digital representation of a legal, contractual, or economic claim connected to that asset, and it is usually not the asset itself.

This distinction sounds academic until you try to redeem something. When you hold a tokenized money market fund, you generally hold a fund share recorded as a token, not a pile of Treasury bills in your name. When you hold a gold token, you hold a claim against whoever custodies the bullion, under terms set by the issuer. The blockchain records who holds the token and tracks transfers, but the enforceability of the underlying claim still depends on off-chain documents, custody arrangements, and the law of some jurisdiction. Tokenization changes the plumbing. It does not rewrite the legal nature of what sits underneath.

This is also where RWAs sit inside the wider world of decentralized finance. If the terms here feel unfamiliar, our mechanism-first guide to what DeFi actually is, layer by layer explains the stack that RWAs plug into, and where real-world trust re-enters an on-chain system.

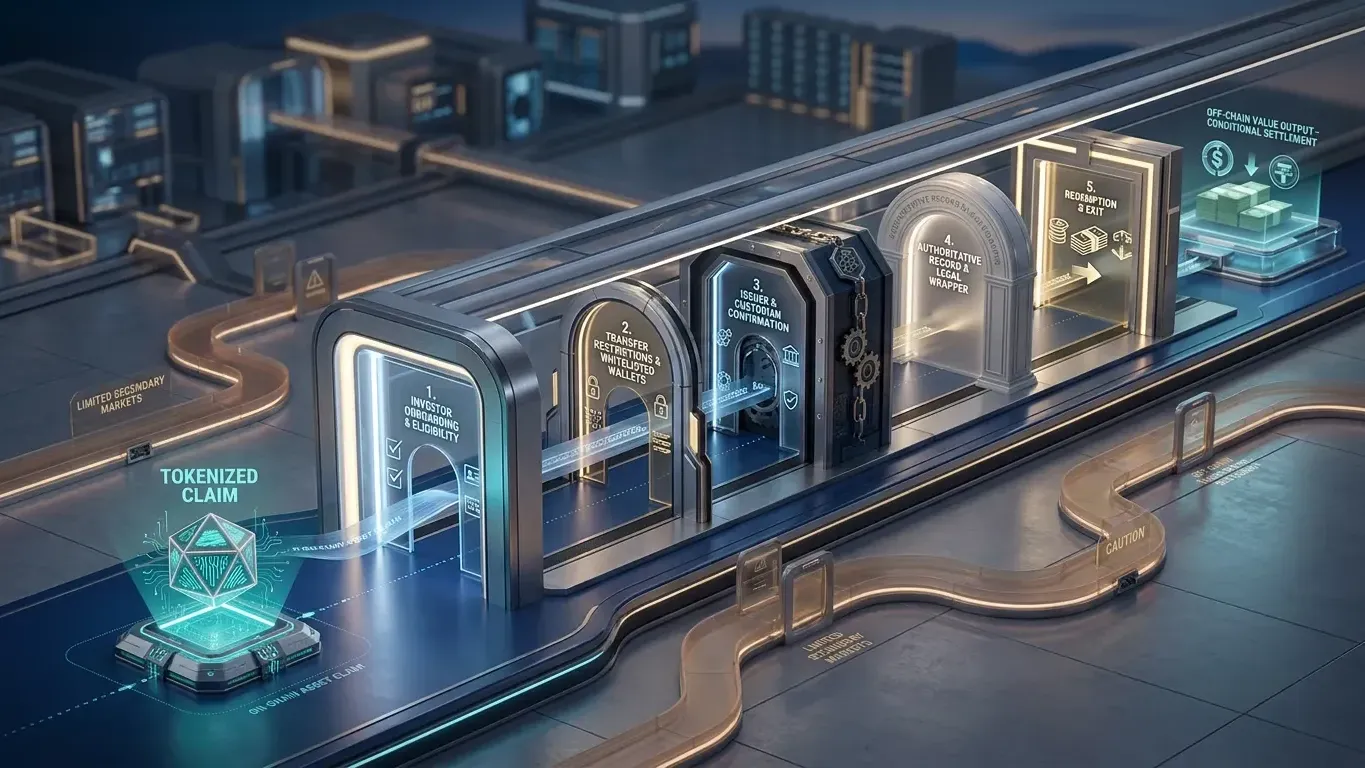

How a real-world asset becomes a token

Turning an asset into a token is not one action. It is a stack of legal and operational steps, and each layer answers a different question a careful reader should be asking. The token most people see is only the visible top of that stack.

The RWA Claim Stack: How an Off-Chain Asset Becomes a Token

Framework: educational synthesis based on ECB, IOSCO, SEC, and issuer disclosures cited in this article. Notes: simplified for beginner education. Exact structures vary by product.

Notice how much of that stack lives off-chain. Smart contracts handle minting, transfers, and sometimes yield distribution, which is the part that feels new. But the issuer, the custodian, the transfer agent, and the redemption terms are traditional financial-market machinery. That is the part most hype-led explainers gloss over, and it is the part that decides whether your claim is worth anything.

This matters because the failure points are concrete, not theoretical. If the issuer becomes insolvent, if the custodian mishandles the asset, if the on-chain record and the official register disagree, or if redemption is gated during stress, the token in your wallet does not save you. Understanding the stack is the difference between reading a token as proof of ownership and reading it as one link in a chain of promises that each need to hold.

What is actually live in 2026

The live RWA market is real, and it has grown quickly, but it is smaller and more concentrated than the trillion-dollar forecasts suggest. According to RWA.xyz market data, the on-chain value of tokenized real-world assets, excluding stablecoins, stood at roughly 31.7 billion dollars as of July 1, 2026, up from around 6.6 billion dollars a year earlier. That is fast growth from a small base, and it sits against traditional markets measured in the tens of trillions.

Tokenized Real-World Assets by the Numbers, 2026

The market is growing fast, but it is concentrated and still early. Read the numbers as scale, not as safety or liquidity.

$31.7B

in total distributed on-chain value of tokenized real-world assets, excluding stablecoins, up from roughly 6.6 billion dollars a year earlier. Large in crypto terms, but small next to the multi-trillion-dollar traditional markets these tokens represent.

50%+

of that value sits in US government-backed instruments such as Treasuries and money market funds. The market is broadening, but concentration in one familiar, low-credit-risk category remains high.

6

asset categories that each independently pass 1 billion dollars on-chain, including private credit, Treasuries, commodities, and corporate bonds. A sign the market is diversifying beyond a single asset class, though most categories are still early.

Sources: RWA.xyz market overview, as of 07/01/2026, rechecked 2026-07-02. Metric: on-chain value and category breakdown of tokenized real-world assets, excluding stablecoins. Notes: distributed asset value differs from represented asset value. Figures are time-sensitive and reported by a single analytics dashboard.

Those numbers describe scale, not safety. A large figure on a dashboard does not prove that an asset is liquid, decentralized, widely accessible, or low risk. It is a starting point for questions, not an answer. With that framing in place, here is how the categories sort by maturity.

Tokenized RWAs in 2026: Live, Restricted, and Still Pilot

The same word, tokenized, hides very different levels of maturity and access. This map sorts them.

Live and strongest

Tokenized money market funds and Treasuries

The clearest live category. BlackRock's BUIDL passed 2.5 billion dollars by late May 2026, and Franklin Templeton's BENJI, WisdomTree's WTGXX, and Ondo's OUSG are established products. Access is usually limited to vetted or eligible investors and approved wallets.

Live but different

Tokenized gold and commodities

Gold-backed tokens such as PAXG and XAUT are easier to picture because the reference asset is physical bullion. Custody, storage, and redemption terms still decide what the token is worth.

Live but gated

Private credit and fund wrappers

Tokenized private credit and alternative fund access exist through regulated feeder structures, but they are generally offered to qualified or accredited investors, not the general public.

Entering production

Regulated market infrastructure

Controlled milestones, not universal plumbing yet. DTC's tokenization service and Securitize's expanded broker-dealer role are moving into production during 2026 under regulatory conditions.

Still pilot or restricted

Broad equities, real estate, retail private equity

High narrative appeal, thin reality so far. Broad retail tokenized stocks, most tokenized real estate, mainstream private equity access, and deep 24/7 secondary markets remain limited or jurisdiction-specific.

Sources: RWA.xyz, ECB (April 2026), DTCC (May 2026), and issuer disclosures cited in this article. Notes: maturity labels are an editorial synthesis. Product access and eligibility vary by jurisdiction.

Take the strongest category first. Tokenized money market funds and Treasury-backed products lead because they are short-duration, cash-like, and familiar to institutions. BlackRock's tokenized fund, issued through Securitize, is one of the largest of these products, and Franklin Templeton has described its fund as the first US-registered money market fund to use a public blockchain as its system of record. These are live, but the fine print matters. WisdomTree's tokenized Treasury money market fund, WTGXX, launched 24/7 trading and instant settlement in February 2026 through a dealer-principal model, using SEC exemptive relief and FINRA approval, with USDC as the initial settlement asset, as the firm's February 2026 announcement describes. The same disclosure notes the fund is not a bank account and is not insured, which is a useful reminder that a live product still carries risk.

There is a reason this corner of the market matured first, and it is worth understanding rather than memorizing. Short-term Treasuries and money market funds are familiar, low-credit-risk, and cash-like, which makes them the easiest traditional instrument to move on-chain without frightening a compliance department. Their yield can be delivered programmatically through smart contracts, and the resulting token can then be used as on-chain collateral, which is genuinely new and useful for institutions managing treasury operations. The harder categories, where legal ownership, valuation, and secondary markets are messier, have not moved nearly as fast, which is the clearest evidence that tokenization follows the underlying asset's complexity rather than erasing it.

The infrastructure layer is the other big 2026 story, and it is genuinely important. In December 2025, the Depository Trust Company received an SEC no-action letter to run a controlled tokenization service for assets it already custodies, including the Russell 1000, major index ETFs, and US Treasuries. DTCC later confirmed the rollout timeline in its May 2026 update, with limited production trades planned for July 2026 and a fuller service launch in October 2026. Separately, Securitize said in May 2026 that FINRA's continuing membership process cleared its broker-dealer to custody tokenized securities, run atomic settlement against stablecoins, and take part in underwriting for tokenized offerings, per the company's May 2026 release. These are real regulatory milestones, but the honest description is controlled infrastructure entering production, not a finished 24/7 market for everyone.

Understanding this is not academic. It is the difference between reading a headline as an open door and reading it as a narrow, permissioned pilot. When a cautious reader assumes that a tokenized Treasury behaves like a brokerage account or a stablecoin, the gap between that assumption and the actual product terms is where costly surprises live. The mechanism, not the marketing, tells you what you are really holding.

What is still pilot, restricted, or early

The categories with the most exciting stories are often the least mature. Broad retail access to tokenized public equities exists in several forms, but it is not the default state, and access depends heavily on where you live. Some platforms offer tokenized stock exposure to non-US users without the same protections a domestic brokerage account carries, and the token often tracks a security held by a third party rather than giving direct ownership. Regulators have been clear that these instruments do not escape securities law simply by moving on-chain.

Tokenized real estate is the classic example of narrative running ahead of reality. Fractional property tokens promise easy access, but title transfer, property rights, investor protection, and cross-border enforceability remain slow and jurisdiction-specific. Public-sector initiatives, such as Dubai's real estate tokenization efforts, are worth watching, but this category is better understood as early and localized than as a mature global market. The same caution applies to private equity for ordinary investors, where lockups, eligibility rules, valuation lag, and fees still stand between a token and genuine access.

The hardest problem sits under all of these. Tokenization does not automatically create a market. The European Central Bank's April 2026 analysis of tokenized money market funds found the sector small but expanding rapidly, and its wider review of tokenized markets noted that secondary-market trading remains limited, which restricts liquidity and investor participation. The ECB also warned that tokenized funds could amplify liquidity mismatch and operational fragility, a caution you can read in full in its April 2026 Macroprudential Bulletin. In plain terms, putting an asset on-chain does not conjure buyers for it.

Tokenized does not mean liquid, safe, or owned

Most of the confusion around RWAs comes from a handful of claims that sound reasonable and quietly overreach. Sorting the marketing language from the mechanism is the single most useful skill a beginner can build here. None of these corrections require you to be cynical, only to read one layer deeper than the headline.

RWA Claims Worth Questioning

Myth

If it is tokenized, I own the real asset directly

This collapses the token, the wrapper, and the asset into one thing.

Reality

The token is usually a claim on a fund, note, or wrapper

Your rights come from that legal structure, not from the fact that a token exists on a blockchain.

Myth

Tokenized assets are automatically liquid

Existence on-chain is treated as the same thing as tradability.

Reality

Liquidity depends on buyers, not on tokenization

Whitelisting, transfer limits, market makers, and redemption terms decide whether you can actually sell.

Myth

A tokenized Treasury equals holding a Treasury bill

The label suggests a direct, risk-free government position.

Reality

You usually hold a fund share or note

That product holds or references Treasuries and adds its own issuer, fees, and redemption rules.

Myth

On-chain means outside regulation

Tokenization is imagined as a way around securities law.

Reality

The most credible products sit inside regulated wrappers

US regulators have stated that tokenizing a security does not change the fact that it is a security.

Myth

A large market cap means low risk

Headline size is read as a safety signal.

Reality

Size can hide concentration

Few active holders and thin secondary trading can make a large tokenized asset hard to exit.

Framework: educational synthesis based on SEC, ECB, IOSCO, and issuer sources cited in this article.

The regulatory point deserves emphasis because it anchors the rest. In July 2025, SEC Commissioner Hester Peirce made the case plainly that tokenization does not change the legal nature of an asset, and that a tokenized security is still a security subject to federal securities laws, in a statement you can read on the SEC website. SEC staff reinforced that view in a January 2026 joint statement describing tokenization as a recordkeeping method rather than a legal transformation. This is why serious RWA products tend to look like regulated financial-market infrastructure rather than a permissionless escape from it.

There is a common beginner mistake buried in all of this, and it is an understandable one. Many people judge a tokenized asset the way they judge a crypto token, by looking at its market cap and its yield. This happens because those are the numbers most visible on a dashboard. But for an RWA, the more important questions are what the token represents and whether you can actually redeem it, and those answers live in the product documents, not the price chart. A checklist of small crypto habits that trip up newcomers is collected in our guide to the most common crypto mistakes beginners make, and this one belongs on the list.

RWAs are not stablecoins, even when they use them

Category confusion is one of the biggest sources of RWA misunderstanding, so it helps to separate four things that often get blurred. A stablecoin is a token designed to track a fiat value, backed by reserves held by an issuer. A tokenized deposit is a commercial bank deposit represented on-chain, which is a claim against a regulated bank. A tokenized RWA is an off-chain asset, fund, or claim represented on-chain, where your rights depend on the wrapper. A native crypto asset, such as ether, is native to a blockchain and is not backed by an off-chain asset in the same way.

These lines blur in practice because RWAs frequently use stablecoins as the settlement asset for buying and redeeming. A tokenized Treasury fund might settle against a stablecoin, which means the payment leg and the asset leg are two separate promises that both have to hold. If you want the deeper comparison of on-chain money types, our explainer on the difference between tokenized deposits and stablecoins covers who controls each rail. The short version is that the token you hold and the token you settle in can have very different risk profiles, and a good habit is to ask about both.

How to evaluate an RWA claim before trusting it

You do not need a law degree to think clearly about a tokenized asset. You need a short, repeatable set of questions that force the marketing language to explain itself. Blockready's DeFi module works through tokenized real-world assets alongside stablecoins, liquidity pools, and lending as separate learning steps, because these concepts are easy to blur when they are taught too quickly, and RWAs sit right at the intersection.

Questions to Ask Before Trusting an RWA Claim

Framework: educational synthesis based on SEC, ECB, IOSCO, and issuer disclosures cited in this article. Notes: educational checklist, not investment, legal, or tax advice.

This is the same discipline that sits behind any serious evaluation habit. The point is not to memorize product names, which change constantly, but to build a reflex of asking what a token gives you before asking what it might return. If that reflex feels familiar, it is the same one behind our structured DYOR framework for crypto due diligence, applied to an asset class where the legal and custody questions carry even more weight. When a term in a product document is unfamiliar, it is worth pausing to look it up in a reliable crypto glossary rather than guessing.

Based on how we sequence the curriculum, our view is that RWAs are best learned after self-custody, stablecoins, and settlement, not before. A tokenized asset is a claim wrapped in legal and operational layers, and those layers only make sense once the basics underneath them are clear. We do not recommend treating a tokenized Treasury as a cash-equivalent or a stablecoin substitute for anyone who has not checked the wrapper, the issuer, and the redemption terms, because the reassuring label hides exactly where the risk sits. That is not a criticism of the products. It is a consequence of how many promises stack up between the token and the asset.

The core idea

The useful question about a tokenized real-world asset is not whether it is on-chain. It is what claim the token gives you, who stands behind that claim, and how you get your money back. Tokenization can improve settlement and operations, but it does not remove the issuer, the custodian, the legal wrapper, or the rules that govern them.

For an enterprise or a team, the same literacy shows up as an operational and compliance question rather than a personal one. RWAs in 2026 look less like a permissionless crypto rebellion and more like regulated capital-markets infrastructure being rebuilt on new rails, which is why custody, transfer agents, broker-dealers, and settlement assets keep appearing in the story. A team that understands that stack can evaluate a tokenization vendor or product with the right questions instead of the wrong assumptions. That is the difference between adopting a technology and understanding it.

Frequently Asked Questions

What are tokenized real-world assets?

Tokenized real-world assets are off-chain assets, such as money market funds, Treasuries, gold, private credit, or shares, represented on a blockchain as digital tokens. The token is usually a claim on the asset or a fund, recorded and transferred on-chain, rather than the physical asset itself.

Is a tokenized asset the same as owning the actual asset?

Usually not directly. In most products the token represents a legal or economic claim, such as a fund share, note, or receipt, and your rights depend on that wrapper and on off-chain custody and law. The blockchain records the transfer, but it does not by itself grant direct title to the underlying asset.

Are tokenized real-world assets safe?

Tokenization does not make an asset safe by itself. It replaces some crypto-native risks with issuer, custody, legal, redemption, and regulatory risks, and it adds smart-contract and settlement risk on top. The safest-looking products, such as tokenized money market funds, still carry risk and are generally not insured like bank deposits.

Are tokenized assets automatically liquid?

No. A token can exist on-chain and still have few eligible buyers. Liquidity depends on whitelisting, transfer restrictions, market makers, redemption terms, and available settlement assets, and the European Central Bank noted in April 2026 that secondary-market trading in tokenized assets remains limited.

How are RWAs different from stablecoins?

A stablecoin is designed to track a fiat value and is backed by reserves, while a tokenized RWA represents a broader asset such as a fund, bond, or commodity, with rights that depend on its wrapper. RWAs often use stablecoins as the settlement asset for buying and redeeming, which means the token you hold and the token you settle in can carry different risks.

What types of real-world assets can be tokenized?

The most established live categories in 2026 are tokenized money market funds, Treasury-backed products, and tokenized gold, with private credit and alternative fund wrappers live but restricted to eligible investors. Broad retail tokenized stocks, most real estate, and mainstream private equity access remain limited, jurisdiction-specific, or pilot-stage.

Build Your Team's Tokenization and Compliance Literacy

Blockready's enterprise solution helps teams build blockchain and crypto literacy through structured training, assessment, progress tracking, and continuously updated content, so your organization can evaluate tokenized assets with the right questions instead of the wrong assumptions.

Explore Enterprise Training